05 Jun Employee Retention Credit for Employers Affected by Hurricanes Irma and María

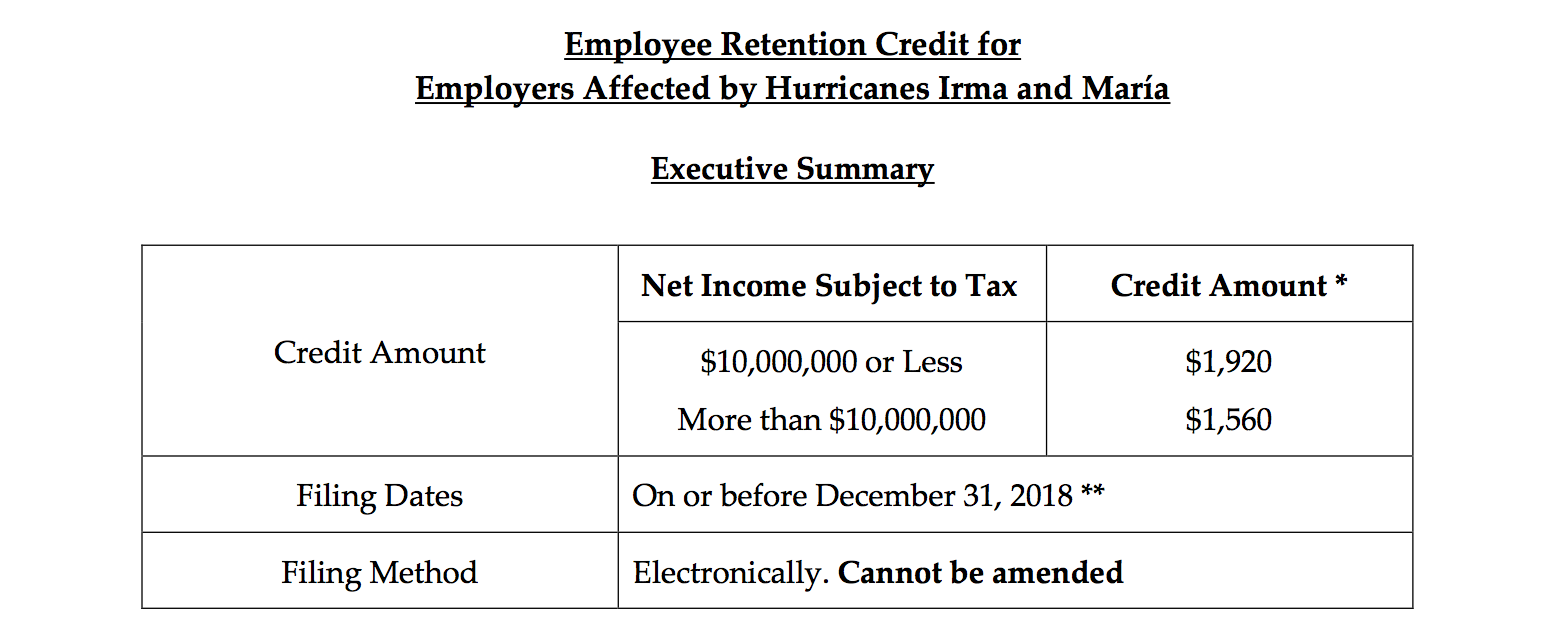

* Certain requirements and conditions apply. Please see below for more information. ** Portal was supposed to be available as of June 1, 2018; however, it is not operational yet. We understand it shall be available in the next following days.

Background

The Disaster Tax Relief and Airport and Airway Extension Act of 2017 was signed by President Trump on September 29, 2017 (hereinafter “Act”) to provide targeted tax relief for taxpayers impacted by Hurricanes Harvey, Irma, and María. Among the reliefs provided by the Act, there is a tax credit of the applicable percentage of 40% of the qualified wages paid by disaster-affected employers to each employee from a core disaster area. The credit was made extensive to businesses that are operating in Puerto Rico with certain changes and adjustments. Bear in mind that, contrary to Puerto Rico, in the case of a US employer who files Federal income tax returns, it is NOT a refundable credit and any credit granted would reduce the salaries deduction in the federal tax return.

General Rules in the US

Generally, the total amount of qualified wages for the determination of this credit is limited to $6,000 per employee. It means, that the maximum credit amount would be $2,400 per employee. As noted below, the credit per employee in Puerto Rico has been reduced. As a general guidance for federal tax purposes regarding this tax credit, we can mention the following:

- It is added to the General Business Credit (which usually is not refundable) in the determination.

- It will apply if the business is inoperable as a result of the damages sustained by Hurricanes Irma and María.

- Qualified Wages means salaries actually paid while the business was inoperable.

- A business may be considered inoperable if, for example, and as a result of the damages sustained by the Hurricanes, the business is physically inaccessible to employees, raw material, utilities or customers.

- The amount of the credit is subtracted from the deduction of wages because the employer did not have the economic burden of said payment.

- This type of benefit has been used before, and this formula for the credit computation was originally created with Hurricane Katrina in 2005.

- Note that tax disaster relief legislation is usually of a temporary nature, therefore no official regulation has been issued on this matter, however some guidance has been provided by administrative publications and letters.

Applicable Rules in Puerto Rico

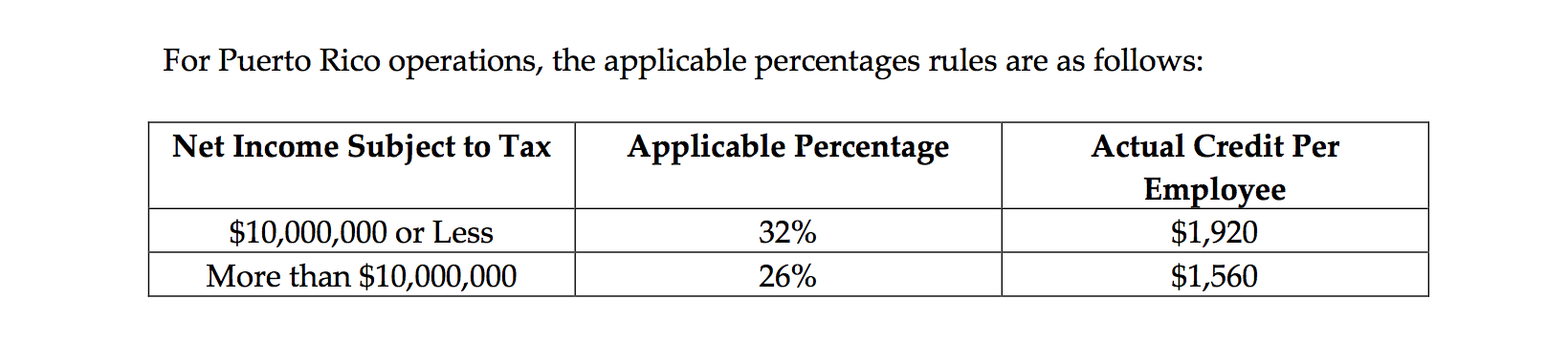

Amount of the Applicable Percentage – The Applicable Percentage for the computation of the credit in Puerto Rico will not be 40%. This adjustment was made due to the fact that Puerto Rico Businesses do not file a Federal Income Tax Return.

Comments:

- The computation of net income subject to tax is done per taxpayer; therefore no aggregation is required in the case of controlled or affiliated groups.

- The Actual Credit Per Employee was computed assuming $6,000 or more were paid in salaries to the employee during the period the business was inoperable.

Eligible Salaries – Eligible Salaries means salaries paid to an Eligible Employee during the time the business was inoperable. The maximum amount of Eligible Salaries shall be $6,000 per employee. Even though the Island was subject to two hurricanes, the total amount shall be limited to $6,000 per employee and should not duplicate salaries. It includes all types of remuneration including back pay, vacations and sick days.

Eligible Employees – Means persons that were employees prior to the passing of the Hurricanes. The provision also requires that Puerto Rico was the main place of employment for such employees. The owner of the entity and his/her close relatives shall not be considered eligible employees. The owner is defined as any person who owns 51% or more of the business.

Inoperable Business – It means the period of time that the business was not able to operate because of Hurricanes Irma and María. The period of time cannot be extended after December 31, 2017. The determination for Hurricane Irma would only cover the following municipalities: Canóvanas, Cataño, Culebra, Dorado, Fajardo, Loíza, Luquillo, Toa Baja, Vega Baja, and Vieques.